The steps in the accounting cycle are fundamental processes that businesses use to track their financial transactions and prepare accurate financial statements. It encompasses a series of steps that enable organizations to record, analyze, and report their financial information. Understanding the steps in the accounting cycle is crucial for maintaining accurate financial records and making informed business decisions. In this article, we will delve into each stage of the accounting cycle and explore its significance in financial management.

Table of Contents

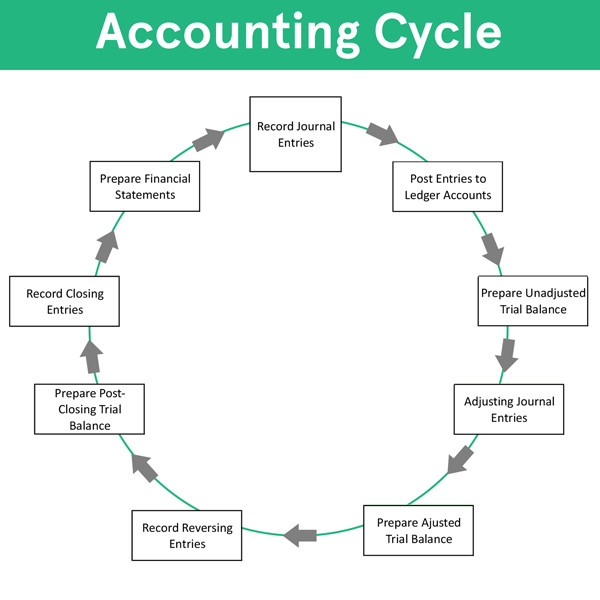

Identify and Analyze Transactions

The first steps in the accounting cycle is to identify and analyze transactions. During this stage, businesses examine their financial activities, such as sales, purchases, and expenses. The goal is to determine the impact of these transactions on the company’s financial position. Accountants review supporting documents, such as invoices and receipts, to gather relevant information and classify transactions into appropriate accounts. By analyzing transactions, organizations gain valuable insights into their cash flows and overall financial health.

Journalize Transactions

Once transactions are identified and analyzed, they need to be recorded in a journal. In this step, known as journalizing, accountants enter transaction details in chronological order. Each entry includes the date, accounts involved, and the corresponding amounts. Journalizing provides a comprehensive record of all financial activities, making it easier to track and analyze transactions later. This step ensures that no financial information gets overlooked and facilitates accurate bookkeeping.

Post to the General Ledger

After journalizing transactions, the next steps in the accounting cycle them to the general ledger. The general ledger contains individual accounts where transactions are summarized. Accountants transfer information from the journal to the appropriate accounts in the ledger. This process involves updating both the debit and credit sides of the accounts, ensuring that the accounting equation (Assets = Liabilities + Equity) remains balanced. Posting transactions to the general ledger provides a consolidated view of all financial activities, facilitating accurate financial reporting.

Prepare a Trial Balance

Once transactions are posted to the general ledger, businesses prepare a trial balance. A trial balance is a summary of all account balances, both debit and credit. It ensures that the total debits equal the total credits and serves as a preliminary check for accuracy. If the trial balance does not balance, it indicates an error in recording or posting transactions. By identifying discrepancies early on, steps in the accounting cycle can rectify errors and maintain accurate financial records.

Adjusting Entries

At the end of an accounting period, businesses need to make adjusting entries to ensure that financial statements reflect the correct financial position. Adjusting entries account for items that are not captured in daily transactions, such as accrued expenses or prepaid income. By making these adjustments, organizations accurately allocate revenues and expenses to the appropriate accounting periods, providing a more realistic picture of their financial performance.

Prepare Financial Statements

After making adjusting entries, businesses can prepare their financial statements. The main financial statements include the income statement, balance sheet, and cash flow statement. These statements provide essential information about a company’s profitability, assets, liabilities, and cash flows. By presenting accurate and timely financial statements, organizations can assess their financial performance and communicate it to stakeholders.

Closing Entries

Closing entries are made at the end steps in the accounting cycle period to reset revenue, expense, and dividend accounts to zero. By transferring these balances to the retained earnings account, businesses ensure that the next accounting period starts with a clean slate. Closing entries facilitate accurate financial reporting and prevent revenue or expense carryovers from one period to another.

Recording Transactions in the Journal

Once transactions have been identified and analyzed, the next crucial step in the accounting cycle is to record them in the journal. The journal serves as a chronological record of all financial transactions, providing a detailed account of each entry. Accountants carefully document the date, description, and amounts involved in the transaction.

By recording transactions in the journal, businesses can maintain an accurate and organized record of their financial activities. This step ensures that no transaction is overlooked or omitted, promoting transparency and accountability in financial reporting. Additionally, the journal serves as a valuable reference for future analysis and auditing purposes.

Accountants follow a standardized format when journalizing transactions. Each entry typically consists of the date, the steps in the accounting cycle affected by the transaction, and the respective debit and credit amounts. This double-entry system ensures that the accounting equation remains in balance and allows for accurate tracking of financial transactions.

Properly recording transactions in the journal is vital for maintaining accurate financial records. It provides a clear and detailed account of each transaction, allowing for easy retrieval and analysis. By diligently journalizing transactions, businesses can streamline their bookkeeping processes and ensure the integrity of their financial information.

Conclusion – steps in the accounting cycle

The accounting cycle is a systematic process that enables organizations to record, analyze, and report their financial transactions. By following the steps in the accounting cycle, businesses can maintain accurate financial records, make informed decisions, and comply with regulatory requirements. Each stage of the cycle serves a specific purpose and contributes to the overall integrity of financial information. From identifying and analyzing transactions to preparing financial statements, each step plays a vital role in managing a company’s finances effectively. By understanding and implementing the accounting cycle, businesses can enhance their financial management practices and ensure the accuracy and reliability of their financial information.

Learn about: Empower with valuable financial skills through stock market education for kids. Set them up for a prosperous future today!